Abstract

Africa’s recent strong growth figures allowed to talk about the continent’s “rise” opposed to the previous “hopeless continent rhetoric”. This provides global actors with opportunities to create markets, establish brands, shape industry structures, influence customer preferences, and establish long-term relationships with African states. Withal, however, growth indicators don’t mean successful implementation of “policy reform” and strengthening the governance. The African economies largely remain rent dependent, and in the global economic and financial system, Africa remains the weaker partner. Moreover currently only 4 per cent of Africans have an income in excess of $10 a day. Thus the key question remains: how can African leaders take advantage for the benefit of the ordinary citizen. So far the only “solution” in place is a diversification of dependency which is indeed not a coherent development project for the continent. The current pattern of growth in Africa is neither inclusive nor sustainable — a model of development that is based on enlarging the opportunities for non-commodity production and a rejection of the tyranny of comparative advantage is required.

Until recently, Africa was depicted as the “hopeless continent” (The Economist, May 13th, 2000), a spatial entity supposedly in ‘the limbo of the international system, existing only at the outer limits of the planet which we inhabit’ (Bayart, 2000: 217). Studies have concentrated on how and why the continent has been in a state of “permanent crisis” or exists in a milieu dominated by conflict, poverty, disease and criminality. From this it has been easy to move to the next step of believing that the continent does not have any significant politics, only humanitarian disasters.

Globalization presses a core challenges to many historical assumptions. Since the 1990s the global governance system, which is based on the power architecture of the United Nations, has been pushed by the global community for years to modify. However the system, built as an outcome of World War II, has remained rigid. This is largely supported by the opposition by the most powerful states and those, particularly Western actors, that would find themselves in an uneven and less influential position within international organizations that would no longer correspond to their immediate post-World War II profiles. Some emerging powers have been among the most active in pressing for the beginning of changes. Nowadays, they are not powers that can be simply ignored. The need for modification in global governance is thus increasingly pressed.

As powers such as Russia and China, and emerging powerhouses such as Brazil, and India have gained political and economic weight at the international level, this has resulted in the diminishing effectiveness of the global governance institutions in which Western states play an important role relative to the strength of the other powerful states. At the same time, it has meant a relative increase in the role that these emerging powers are playing in Africa.

Given Africa’s recent strong growth figures, a perceptible shift has now moved in the opposite direction. Africa has now moved from one extreme to another and is now the “rising star” ( The Economist, December 3, 2011). In late 2012, Time magazine’s December 3rd edition was emblazoned with the headline, “Africa Rising”, capturing a certain l’esprit du temps in some quarters. Other observers now argue that we are living in ‘Africa’s moment’ (Severino and Ray, 2001), where it is ‘Africa’s turn’ (Miguel, 2009). In this new world, ‘Africa emerges’ (Rotbe rg, 2013), moving from ‘darkness to destiny’ (Clarke, 2012), where it is ‘leading the way’ (Radelet, 2010). In fact, we are told, ‘The Next Asia Is Africa’ (French, 2012: 3), based on an “African Growth Miracle” (Young, 2012). In its more excitable moments, we are even told ‘Why Africa will rule the 21st century’ (African Business, January 2013: 16). Previous studies on the political economy of Africa are now dismissed as “Afro-pessimism”, to be swept away by this new Africa: ‘The Ultimate Frontier Market’ (Matean, 2012). A recent book on ‘the story behind Africa’s economic revolution’ even has a quasi-Superman springing from Africa on its front cover (see Robertson, 2012). In short, ‘It’s time for Africa’ (Ernst and Young, 2011).

New governance – opening the Potential

As part of such dynamics, there are claims that huge improvements in governance across Africa have occurred, no doubt to reassure nervous investors. Emblematically, Yvonne Mhango of Renaissance Capital confidently claims that ‘Governments [in Africa] have got policy spectacularly right and created the low-debt, low-inflation, much-improved macro conditions that have enabled growth to take off’. It is not just asset managers spinning this story though. Recently, Ellen Johnson Sirleaf, President of Liberia, stated that ‘In ten years [a] rapidly transforming Africa will move into the industrial age’.

‘Africa’s growth acceleration was widespread, with 27 of its 30 largest economies expanding more rapidly after 2000. All sectors contributed, including resources, finance, retail, agriculture, transportation and telecommunications. Natural resources directly accounted for just 24 percent of the continent’s GDP growth from 2000 through 2008. Key to Africa’s growth surge were improved political and macroeconomic stability and microeconomic reforms. Future economic growth will be supported by Africa’s increasing ties to the global economy. Rising demand for commodities is driving buyers around the world to pay dearly for Africa’s natural riches and to forg e new types of partnerships with producers. And Africa is gaining greater access to international capital; total foreign capital flows into Africa rose from $15 billion in 2000 to a peak of $87 billion in 2007 (McKinsey, 2010). Africa’s economic growth is creating substantial new business opportunities that are often overlooked by global companies. MGI projects that at least four groups of industries — consumer-facing industries, agriculture, resources, and infrastructure — together could generate as much as $2.6 trillion in revenue annually by 2020, or $1 trillion more than today.

Today the rate of return on foreign investment in Africa is higher than in any other developing region. Early entry into African economies provides opportunities to create markets, es tablish brands, shape industry structures, influence customer preferences, and establish long -term relationships. Business can help build the Africa of the future. The rise of the African urban consumer also will fuel long-term growth. Today, 40 percent of Africans live in urban areas, a portion close to China’s and continuing to expand. The number of households with discretionary income is projected to rise by 50 percent over the next 10 years, reaching 128 million. By 2030, the continent’s top 18 cities could have combined spending power of $1.3 trillion.’(McKinsey Global Institute, Report, 2010).

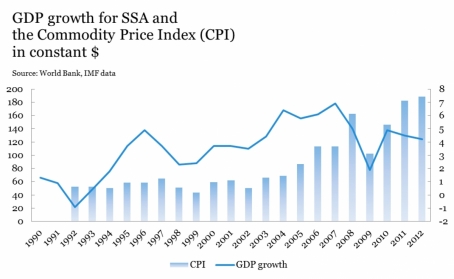

However, the empirical evidence on growth and policy related indicators is consistent with the null hypothesis that more than twenty years of so-called policy reform had limited impact on strengthening the potential for rapid and sustainable growth in the sub-Saharan region. The drivers of the brief recovery during the second half of the 2000s appear to have been a commodity price boom, debt relief and a decline in domestic conflicts. According to SIPRI, the decade had seen a decline in major armed conflicts in Africa. In 1999 there were 11 conflicts ongoing in Sub-Saharan Africa, but by 2009 this had declined to 4[1]. World Bank figures with regard to the annual percentage growth rate of GDP at market prices, based on constant local currency (for all income levels, rounded up), compared to the movement of the Commodity Price Index reveals this intimate link:

The years when SSA’s growth figures surpassed 1996 levels (2004-2008) can be demonstrably linked to the period when China and India (and other emerging economies) began to hugely demand commodities, as reflected in the CPI. In the energy realm, concern over predicted declines in petroleum reserves, apprehensions over the so-called “peak oil” scenario, instability in the Middle East and oil price speculation placed further pressure upwards on prices, peaking in 2008 (only to tumble after the core underwent the worst recession in a century). This reality is qualitatively different from the picture Goldman Sachs, Renaissance Capital et al. portray, where ‘spectacularly right’ policies have driven growth. Official reports from international organisations have at times bolstered this latter interpretation, postulating Africa’s “economic resurgence” as being hinged on the ability of the continent to recover from the global crisis relatively quicker than other areas of the world. Whilst true in and of itself, Africa’s growth record over the last ten years or so has occurred within the context of overall global growth. In this regard, Africa’s growth has only been around 1 per cent higher than the world average: credible, but not fantastic.

An interesting by-product of the “Africa Rising” narrative are the wild claim about Africa’s middle class, with assertions that it now amounts to over a third of Africa’s population. It emerges that this figure was arrived at by calculating the number of people estimated (using dubious statistics) to have a per capita consumption between $2 and $4. This criteria itself sets the bar at an incredibly low level, but of course then allows the ADB to add its voice to the narrative that the dawn has arrived and that the corner has been turned etc. In fact, currently only 4 per cent of Africans have an income in excess of $10 a day.

We have heard all this noise about Africa’s immanent renaissance before —on multiple occasions. It is ironic that Time magazine’s late 2012 edition celebrated “Africa Rising”, given that fourteen years earlier (March 30, 1998, to be precise), Time ran a story with the exact same title! Then, we were told that ‘Hope is Africa’s rarest commodity. Yet buried though it is amid the despair that haunts the continent, there is more optimism today than in decades’. Better times are always coming tomorrow (passages from various World Bank reports):

From a 1981 World Bank report, Accelerated Development in Sub-Saharan Africa (p. 133): ‘Policy action and foreign assistance…will surely work together to build a continent that shows real gains in both development and income in the near future’. From a 1984 World Bank report, Toward Sustained Development in Sub-Saharan Africa (p. 2): ‘This optimism can be justified by recent experience in Africa…some countries are introducing policy and institutional reforms’. From a 1986 World Bank report, Financing Growth with Adjustment in Sub-Saharan Africa (p. 15): ‘Progress is clearly under way. Especially in the past two years, more countries have started to act, and the changes they are making go deeper than before’. From a 1989 World Bank report, Sub-Saharan Africa: From Crisis to Sustainable Growth (p. 35): ‘Since the mid-1980s Africa has seen important changes in policies and in economic performance’. From a 1994 World Bank report, Adjustment in Africa (p. 3): ‘African countries have made great strides in improving policies and restoring growth’. From a 2000 World Bank report, Can Africa Claim the 21st Century?: ‘Since the mid-1990s, there have been signs that better economic management has started to pay off’. From a 2002 World Bank press release on African Development Indicators, ‘Africa’s leaders…have recognised the need to improve their policies, spelled out in the New Partnership for African Development’.

In 2008 Africa was at a “Turning Point”, restated in 2011 with the assertion that the continent was ‘on the brink of…economic take-off, much like China was 30 years ago’.

Africa’s Turning Point or Bargaining for a New Position?

The real story as it pertains to contemporary excitement about Africa seems to be in the upsurge of interest in Africa by formerly non-traditional actors. The emergence in 2009 of BRICS – Brazil, Russia, India, China and South Africa — platform generated a lot of discussion about the political, economic and even social impact of this diplomatic club on the transformations currently taking place in the world. The group has immense economic power in that it brings together countries whose populations constitute 43 per cent of the world population, whose territories make just over a quarter of the world’s land area, whose combined GDP accounts for 21 per cent of the world’s GDP, and whose reserves are huge at about US$3 trillion.

Demand for multilateral diplomacy and the collaborative leadership of most influential countries strongly increases in the world when there is need to solve the urgent challenges and answer common threats and problems. Recent developments, such as the unrest in the global economy, only demonstrates the ineffectiveness of existing organs to monopolize global governance and address all the issues from a single centre. In a world increasingly aware of the need for the deideologization of international affairs, the strengthening of the legal fundamentals of the international system are vitally needed.

High economic growth in Africa must be understood in the context of the rise in importance of various “emerging powers” within the global political economy. The relationship that these “new” powers have with Africa has elevated the continent in the strategic thinking of the extant “traditional” (largely ex-colonial) partners. As one French minister was quoted as saying, ‘Thanks to the Chinese, we [have] rediscovered that Africa is not a continent of crises and misery, but one of 800-million consumers’. Though this comment was directed at the “rise” of China in Africa, it might be equally applied to relatively new sets of economic and political linkages. Embedded in ‘a fluid period of transition in the global balance of power and the international state system characterised by traditional and emerging powers’, the continent now plays a more prominent role in international.

Africa has ‘never been in such a strong bargaining position’ than at the p resent, with numerous ‘suitors’. The growing diversity of partners potentially offers a ‘tremendous opportunity’, ‘as each country brings with it an array of capital goods, developmental experience, products and technology as well as new opportunities to trade goods, knowledge and models’. Trade with—and investment from — emerging economies potentially reduces the North’s political leverage and economic dominance in Africa, which may ‘increase the negotiating power enjoyed by [African] governments seeking to maximise local benefits’.

Decades after the European powers carved up the African continent for their own imperial needs, Africa is undergoing a new wave of resource and strategic exploitation – some are calling it the new scramble for Africa. The United States is increasing its footprint across Africa with AFRICOM, fighting terrorism and ensuring stability are the trumpeted motivations. Resource security is a more hushed objective. But it is not just about the US. During the last decade, China’s trade wit h Africa not only caught up with America’s, it has more than doubled it. The new battle for Africa does not deploy strong-arm tactics, it is now using economic and humanitarian aid, interest-free loans, preferential trade agreements and investments in infrastructure. These are a useful currency across a continent that is, for the world’s established and emerging powers, seemingly up for grabs. India, Brazil and Russia are all invested in Africa’s present and future, and old imperial powers like France are fixing to retain their loosening grip on the riches of former colonies.

China is now Africa’s biggest business partner, with roughly $200bn (£120bn) in trade in 2013 – more than double the trade that Africa did with United States, which is also behind Europ e. More than one million Chinese migrants have moved to Africa to help the cause. That speaks volumes. What started as insatiable demand from China for Africa’s rich seams of commodities – which involved the Chinese moving in to build the massive infrastructure and transport links required to get the resources out of Africa – has developed into a much broader trading relationship in all sorts of goods and services.

Africa however remains the weaker partner. The weakness is usually ascribed to the continent’ s dependent relationship in the international system and Africa’s historic insertion into the global capitalist economy. However, dependence is ‘a historical process, a matrix of action’, that permits the prospect of alteration stemming from changes in the dynamics, processes and organisation of the international system and the fundamental tendencies within Africa’s political economy. Current emergent trends, such as robust economic growth and an increasing diversification of the continent’s international relations may play important roles in this regard, yet massive challenges remain. Africa’s world market share in processing industries is extraordinarily low: SSA exports just 0.9 and 0.3 per cent of world light and heavy manufacturing exports respectively. The bulk of the growth in African exports in the last decade or more has been heavily underpinned by mining -related commodities, deeply problematic in terms of development. After all, the export growth that the Asian economies used to leapfrog development was based on an increasing list of manufactures. Africa is nowhere near that position.

Yet it is true that actors from both the global North and South are now actively pursuing closer engagement with Africa. This provides the elites of the continent oppor tunities to extract leverage in return for access. This may or may not be a good thing, depending on the conjectural circumstances in each state formation and the nature of the external partners. It cannot be taken for granted that actors such as the BRICS are interested in furthering Africa’s developmental priorities. Though Africa has possibly never been in a stronger bargaining position than at present, the key question remains: how can African leaders take advantage for the benefit of the ordinary citiz en. Currently, this does not seem to be happening. A recent Afrobarometer survey revealed that despite a decade of strong GDP growth and the incessant narrative of an “Africa Rising”, ‘there is ‘a wide gap in perceptions between ordinary Africans and the global economic community’, where ‘a majority (53%) rate the current condition of their national economy as “fairly” or “very bad” and only ‘one in three Africans (31%) think the condition of their national economies has improved in the past year, compared to 38% who say things have gotten worse’. Notably, when it came to their own elites, ‘Africans give their governments failing marks for economic management (56% say they are doing “fairly” or “very badly”), improving the living standards of the poor (69% fairly/very badly), creating jobs (71% fairly/very badly), and narrowing income gaps (76% fairly/very badly)’ (Hofmeyr, 2014). Popular opinion is thus increasingly out of sync with the “Africa Rising” narrative that has been gaining traction among government officials and international investors.

The question of levels of agency is something that needs to be at the forefront of any discussion on the role of the BRICS in Africa and the potentialities of these emerging relationships in fostering development. This is highly contingent on a variety of contextual factors and it is these dynamics that need to be borne in mind when reviewing each BRICS member’s interaction with the continent.

Emerging countries’ trade structures with Africa do not exhibit any exceptionalism and are comparable to the relationships established by the capitalist core since the colonial period, following the model of the ‘small colonial open economy’. The trade between the BRICS and Africa is clearly dominated by the exportation of commodities. ‘For all the three emerging econ omies, Africa is a major supplier of natural resources. Mineral fuels account for 70% of Africa’s exports to China, 80% of exports to India and 85% of exports to Brazil. This is comparable to African exports of mineral fuels to the US that account for over 83% of the total export basket’. It is not impossible that accrued revenues may help implement constructive change, perhaps in the direction of the welfare reforms pursued by some Middle Eastern oil producers. It is just unlikely.

What Defines the Play? – Oil and Gas.

In the past two decades, Africa has seen an unprecedented boom in oil and gas investment. With big companies shut out, or deterred from investing in the Middle East, Africa has by contrast offered multinationals relatively lenient terms and extensive access to its oilfields in the past 15 years. The continent has been able to attract money from the biggest supermajors, from ExxonMobil to Shell, looking to exploit its prolific and relatively untapped geology, particularly in the Gulf of Guinea and North Africa. It also has the world’s highest ratio of «light» and «sweet» crude oil, preferred by refiners in big consuming countries, and 83 per cent of its oil resources comes from fields yielding more than 100m barrels.

Problematically, developments elsewhere may well push Africa further down the energy dependency road as, paradoxically, exports to the West (particularly the United States) decline. In the past few years, a radical change in the forecasts for growth in American oil production and oil reserves has taken place. This has sprung from light tight oil (LTO), which includes both crude oil and condensate in all tight formations, including shale basins (LTO is frequently referred to as “shale oil”). Currently, the global oil industry is considering LTO’s potential and its likely implications for oil supply and demand. Oil companies have started to develop unconventional hydrocarbons, successfully bringing to the market several large and under-exploited oil and natural gas liquid resources. American shale/tight oil, Canadian tar sands, Venezuela’s extra-heavy oil, and Brazil’s presalt oil are the main examples. This has meant that the fear of a decline in oil supplies (the “peak oil” thesis), which would then prompt concerns about energy shortages and propel oil prices upwards, possibly leading to “oil wars” has been quietly shelved. There is now little doubt that unconventional resources through the “energy revolution” will satisfy global demand. Instead, the debate now revolves around the speed and price at which these resources can be extracted.

The U.S. Energy Department forecasts U.S. production of crude and other liquid hydrocarbons will average around 11.4 million barrels per day (bpd) by 2014, which would place the Unit ed States just below Saudi Arabia’s expected output for 2013 of 11.6 million bpd. Several forecasts put American production at between 13-15 million bpd by 2020, with the IEA (2012), suggesting that the United States may supplant Saudi Arabia as the world’s largest producer. It should be said at this juncture that Saudi oil is cheaper to tap than tight oil and LTO needs a price above $70 per barrel to be profitable (break-even prices of most tight oil are in the range of $40- $60 per barrel). However, the recent turnaround in the United States’ crude oil production is extraordinary and will have major implications for Africa (and the world). As the United States meets more of its current and future demand for oil from indigenous supplies, imports from traditional suppliers will inevitably fall. This has already started to happen in dramatic fashion.

Nigeria has experienced difficulties in finding alternative destinations for its crude and it has had to cut prices. Indeed, at the start of 2013, weak demand forced Nigeria to sell some cargoes of its oil below the official selling price. This would see Nigeria lose $380,000 on a typical cargo. Consequently, ‘Unprecedented growth in USA gas reserves inevitably eliminates USA as a destination for Nigerian gas’. In addition, the growth in gas reserves helps re-establish the United States as a major producer of industries such as petrochemicals, fertilizer etc., in effect slashing the market options for such products from Nigeria.

Another aspect is that the foregoing underscores the close intimacy between state and oil oriented power or agency, and the nature of the fractional squabbles over oil revenues on a national scale, which imposes centralist logic on the control and distribution of oil rents. The result of a ce ntralist imposition of control from past experience is both the intense horizontal struggles for access to, and control of a larger share of oil rents, but more fundamentally, vertical struggles between the marginalized and oppressed groups and the corrupt foreign capitalists, egocentric politicians or oil elite privileged individuals. These struggles also underpin the privileged class formation process mostly through strategic locationing in the distributive circuits of the politics of the oil -state often carried out through primitive accumulation activities. As such the premium on controlling political power is very high, leaving virtually no incentive or space for the democratization of state -society relations. Such features can be gleaned from politics in Nigeria, Angola, Algeria, Southern Sudan, Sudan, Chad, Gabon and Equatorial Guinea, just among few countries.

What is it that Africa Needs?

How this all fits into discussions about “Africa Rising” is that declining North American imports from African countries will likely create a new alignment in the global oil market. For countries that rely on oil exports for the majority of total annual government revenue and foreign exchange earnings, this is highly problematic. One key way in which such countries may seek to avoid the implications of declining exports to the traditional importers is to shift attention to the emerging economies, specifically Asian buyers (especially China and India). This may not all be smooth however, as African producers that produce light sweet crude may not have large enough market in Asia as several Asian refiners already process heavy crude produced by OPEC members in the Persian Gulf. However, the Asian option seems to be the only one available: the oil minister of Angola, Jose Maria Botelho de Vasconcelos, has in fact argued that ‘Emerging markets like India and China have been growing, and they have absorbed a large part of Angolan exports’. But the “solutions” to the energy revolution thus far simply implies a further intensification of an over-reliance on primary commodities, with the hope that through such a diversification of dependency, the effects of new developments in the oil industry may be mitigated: hardly a sustainable or visionary response.

Indeed, rentier strategies rather than developmental strategies tend to be negative —as the history of Africa’s petro-states testify. What is a more likely scenario is one that reifies a situation that Julius Nyerere commented on over thirty years ago, when he noted that ‘we ar e all, in relation to the developed world, dependent — not interdependent — nations. Each of our economies has developed as a bi-product and a subsidiary of development in the industrialised North, and is externally oriented. We are not the prime movers of our own destiny’. A key issue here is that ‘the production of primary goods for export creates a demand for other activities, notably transport, construction and services, which is incompatible with balanced development and channels the meagre proceeds from t he foreign sale of these commodities into expenditures which do not stimulate the rest of the economy’.

Africa needs to rethink its strategies and find ways and means to make them more compatible with the objective of sustainable development. ‘To sustain economic growth, Africa will need to enhance productivity and competitiveness through investing in infrastructure, technology, higher education and health; broadening the range of and adding greater value to exports; and making the necessary investments in productive sectors and trade facilitation. All these measures require collaboration among stakeholders under the leadership of the developmental state’. A redefinition of growth to include structural transformation is needed á la Kuznets’ definition of a c ountry’s economic growth being ‘a long-term rise in capacity to supply increasingly diverse economic goods to its population, this growing capacity based on advancing technology and the institutional and ideological adjustments that it demands’ (1971). Such a definition puts to shame the crass celebration of Africa’s recent growth rates as symbolising some sort of watershed event for the continent.

Outside of Africa, it has been well documented that structural change – that is, the reallocation of economic activity away from the least productive sectors of the economy towards more productive ones – is a fundamental driver of economic development. But there has been very little evidence on how structural change has evolved in Africa since independence across the continent was achieved half a century ago.

Africa cannot achieve sustained economic growth and transformation without diversifying the sources of its economic growth both on the demand and supply sides of its economies, UNCTAD’s Economic Development in Africa Report 2014 argues. The report says that investment is a major driver of structural transformation, and will be critical for sustaining growth for employment and poverty reduction in Africa over the medium-to long-term. Of course, governance, policies and institutions that generate, utilize and catalyze investment matter enormously. These are key because investment rates in Africa are currently low relative to what will be required to achieve national development goals. Africa has experienced relatively high growth during the past decade but the nature and pattern of this growth has not resulted in more jobs and poverty reduction because consumption has been the dominant driver. Instead, the report says, a consumption -based growth strategy must go hand-in-hand with an increase in investment, particularly investment that which increases the capacity to produce tradable goods, to reduce the likelihood of current account imbalances in the future and to diversify sources of growth on both the demand and supply sides.”

Thus, the current pattern of growth in Africa is neither inclusive nor sustainable. ‘There are various reasons for this. Firstly, African countries are heavily dependent on natural resources as drivers of economic growth. But most of these resources—fossil fuels, metallic and non-metallic minerals—are non-renewable and are being depleted at a very rapid rate with negative consequences for future growth and sustainability. The dependence on resource-based growth is also of concern to African policymakers because commodity prices are highly volatile and subject to the caprices of global demand. Such price instability has negative consequences for investment and makes macroeconomic planning challenging’. In addition, ‘higher resource rents are conducive to more corruption’ which will likely further stimulate numerous neopatrimonial regimes across Africa.

A starting point then is firstly, the correct analysis of Africa’s political economy. In short, independent efforts undertaken from within to achieve self-sustained development. Indeed, ‘the room for manoeuvre available to African actors is dependent on rather particular configurations of power and interests internationally’. Detailed analysis of each state-society complex within Africa and the opportunities and constraints that these engender, when encountering external impulses, are required. Through this, an avoidance of a ‘voluntarist emphasis on agency alone’, and ‘structural pessimism’. The outcome(s) ‘will depend on on-going struggles and those to come: social struggles (local dominated classes against dominating classes in all their political dimensions, international conflicts between the leading blocs in command positions of the states and nations. There are no evident prognoses and different ones are possible’. Given that capitalism is a global system, strategic manoeuvring necessarily must be both national and international.

With this in mind, African civil society needs to recognise that there is a quite definite contradiction between, on the one hand, supporting global free trade and, on the other, committing oneself to somehow changing the rules of the system to ensure greater equity. Instead, African progressive actors need to demand that external relations be subordinated to the logic of internal development and that national development should not be simply driven by the imperatives of worldwide capitalist expansion. Such a stance requires a model of development that is based on enlarging the opportunities for non-commodity production and a rejection of the tyranny of comparative advantage.

Ideally, the rise of “new” actors in Africa such as the BRICS offer potential opportunities for the continent. Increasing competition for Africa’s resources thereby reduces transaction costs and possibly improves Africa’s capacity to gain access to goods and services for more acceptable prices. Secondly, the interest of the new actors in African markets potentially may boost the continent’s economies. The new infrastructure being laid out by Chinese and other actors may help in this regard. After all, without sufficient infrastructure, African countries will never be able to employ the powers of science, technology and innovation to attain developmental goals.

Augmented receipts from commodities, new market opportunities and new financing mechanisms being made available may facilitate greater African agency. But none of this is automatic and whilst it varies from country to country, the prognosis thus far is not encouraging. Few state elites in Africa have the capacity (or will) in place to allocate some of the rents from commodity booms towards the goals of long-term development. This is not to say that Africa’s future is foreclosed, just that the celebratory rhetoric of “Africa Rising” needs ditching.

It hardly needs stating that the diversification of dependency is not a coherent development project for the continent, even if the notion that the BRICS somehow facilitate an escape route from the historic relationships with the North is held. In short, the BRICS are potentially problematic vehicles upon which popular African hopes can be pinned on, unless there are serious and qualitative adjustments by the political class in Africa towards the goal of Africa’s structural transformation. An exercise of African agency in this progressive direction is barely a necessary and certainly not a sufficient condition. Africa’s resources must be taken control of by Africans and used to lessen inequality and promote sustainable development.

Of course, external conditions are not propitious to true development—the WTO makes sure of that with multiple agreements that criminalise industrial policy instruments used previously by the core to nurture domestic capacities. This is likely to lock in the dominant position of t he core capitalist countries at the top of the world hierarchy of wealth, with the BRICS countries expressly hoping to join such elite status. This is but a modern version of List’s “kicking away the ladder”. In such circumstances, a “rise” based on an intensification of resource extraction through diversifying partners, whilst inequality and unemployment increase and deindustrialization continues apace, demolishes the “Africa Rising” narrative. For the continent’s part, there are no external heroes waiting to rescue the continent, the BRICS included: ‘national liberation takes place when, and only when, national productive forces are completely free of all kinds of foreign domination’. That has to be the starting point for addressing what Africa needs and for any true rise of Africa.

Valdai International Discussion Club

[1] Figures from Stockholm International Peace Research Institute SIPRI Yearbook 2000 Stockholm: SIPRI, 2000 and Stockholm International Peace Research Institute SIPRI Yearbook 2010 Stockholm: SIPRI, 2010

- Bayart, J-F. (2000) ‘Africa in the World: A History of Extraversion’, African Affairs, 99.

- Clarke, D. (2012) Africa’s Future: Darkness to Destiny: How the Past is Shaping Africa’s Economic Evolution New York: Profile Books.

- Ernst and Young (2011) It’s Time for Africa: Ernst & Young’s 2011 Africa Attractiveness Survey London: Ernst and Young.

- French, H. (2012) ‘The Next Asia Is Africa: Inside the Continent’s Rapid Economic Growth’, Atlantic Monthly, May 21.

- Hofmeyr, J. (2014) Africa Rising? Popular Dissatisfaction with Economic management Despite a Decade of Growth Cape Town: Afrobarometer.

- Matean, D. (2012) Africa: The Ultimate Frontier Market: A Guide to the Business and Investment Opportunities in Emerging Africa Petersfield: Harriman House Publishing.

- McKinsey Global Institute (2010) Lions on the Move: The Progress and Potential of African Economies London: McKinsey and Company. http://www.mckinsey.com/insights/africa/lions_on_the_move

- Miguel, E. (2009) Africa’s Turn? Cambridge, MA: MIT Press.

- Radelet, S. (2010) Emerging Africa: How 17 Countries are Leading the Way Washington DC: Center for Global Development.

- Robertson, C. (2012) The Fastest Billion: The Story Behind Africa’s Economic Revolution London: Renaissance Capital.

- Severino, J-M. and Ray, O. (2001) Africa’s Moment Cambridge: Polity Press.

- US Energy Information Administration (2014) U.S. Imports by Country of Origin http://www.eia.gov/dnav/pet/pet_move_impcus_a2_nus_ep00_im0_mbbl_m.htm

- Young, A. (2012) ‘The African Growth Miracle’, Journal of Political Economy, vol. 120, no. 4.