The status of global warming has changed considerably over the past two decades since the international community placed the problem of climate change on the agenda for the first time. This was confirmed at the Copenhagen conference of signatories to the UN Framework Convention on Climate Change (UNFCCC) in which more than a hundred countries took part in December 2009. The scope of attendees included the leaders of countries that produce the largest amounts of greenhouse gases (which, according to the international group of experts on climate change, have been the main cause of climatic change at the end of the 20th and the beginning of the 21st centuries). The progress of the conference and its results were commented on in detail by politicians, researchers and journalists, whose opinions on the issue differ dramatically. Let us look at the economic aspect of the problem of climate change, including the shifts that have occurred in assessing its impact.

CLIMATE CHANGE AND SHIFTS IN ASSESSING ITS IMPACT

There are three factors of climatic change that are obviously critical:

First, the problem of climate change has reached a truly global dimension and concerns all countries without exception. Climate is a worldwide phenomenon and it constitutes one of the global public benefits. Hence any climate change has a worldwide economic dimension; the solution of problems related to it requires efforts from all countries and, apparently, from several generations of people.

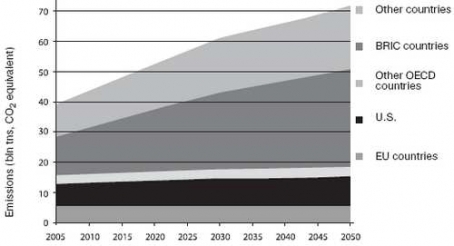

There is a remarkable coincidence of two interrelated tendencies. On the one hand, developing nations are gaining more and more significance in world politics and the global economy, and the current financial and economic crisis has imparted a new impetus to this trend. Many authoritative experts say the crisis has strongly accelerated the shift of economic might from rich countries to developing ones. Since 2007, 45 percent of global economic growth has been provided by BRIC countries (Brazil, Russia, India and China). This figure shows a twofold increase from 2000-2006 and a three-fold increase from the 1990s. On the other hand, developing economies (including Russia) tend to be among the leaders in greenhouse gas emissions (see Graph 1) and, consequently, their role in the solution of this problem is growing visibly.

This is most graphically seen in China – the U.S. and China are the number one emitters of greenhouse gas – a key player at all international talks related to climate change. China’s stance had a most decisive impact on the refusal by participants in the Copenhagen conference to adopt a new binding agreement to replace the Kyoto Protocol, which expires in 2012. As a result, a palliative and rather shapeless Copenhagen agreement was signed.

Graph 1: Dynamics of Greenhouse Gas Emissions

Source: Climate Change Mitigation: What Do We Do? Paris: OECD, 2008, p. 7

At the same time there is a growing awareness that a conclusive resolution to climate problems around the globe is impossible or ineffective. This has been proved, first of all, by the unsatisfactory compliance with the Kyoto Protocol and, second, by the limited efficiency of the Copenhagen conference, which many tend to view as a failure. However, if one considers the steady diversity in the positions of the players, the multitude of the parties involved and the mistrust towards each other, the case in hand seems to be failed or overblown expectations. Solutions to such complicated political and economic problems require transparency of information, trust among nations and a profound reform of international institutions. Naturally, the latter is impossible to attain within the span of several days or even years.

Finally, experts and politicians are becoming more and more aware of the inconsistency of the impact of climate change on different economies, types of people’s activity, and different sections of the population. The reason lies in the irregular pattern of climate change, both in terms of time (its rate has sped up sharply over the past few decades) and space (while globally air temperatures rose 0.8 Celsius from 1900-2005, the figure is almost 50 percent higher for Russia).

The divergence of the consequences that global warming may have for different economies arises from the different degree of vulnerability among countries, industries and population groups to the impact of dangerous natural phenomena. Some may even stand to win from the above-mentioned changes, but the majority will find themselves among the losers. This appears as a crucial circumstance since the key role in efforts to coordinate solutions on mitigating risks from climate change with the tasks of economic development belongs to regional and sectoral economic factors.

Investment in mitigating the risks from climate change is quite substantial. According to World Bank estimates, measures towards reducing greenhouse gas emissions in developing countries alone will require extra – compared to the scenario of the sustained economic model of development based on energy-intensive technologies and use of mineral fuel – capital investment, presumably between $140 billion-$175 billion per year.

Considering the time gap between investment and the benefits derived from it (including the reduction of expenditures owing to energy-saving measures), the scope of this investment is likely to be considerably larger in the first several years. McKinsey consultant experts believe this investment may exceed $560 billion, which means a roughly 3-percent growth compared to the parameters suggested by the inertia scenario of economic development up until 2030. There are fair grounds for this opinion: China alone will have to spend $146 billion annually to reduce greenhouse gas emissions from coal-burning thermal power plants that are the main emitters of these gases.

Given the situation as it is, developing countries can scarcely hope for considerable aid from developed economies, since the latter will have to make large-scale investment in projects for reducing greenhouse emissions themselves. Some assessments suggest that the cost of these projects will amount to $180 billion a year, or roughly the same as in developing nations. Under the Copenhagen agreement, annual aid to developing countries will be $10 billion in 2010-2012, with a possible increase to $100 billion by 2020. Meanwhile, developing countries say the figure should be double or even treble that size.

Investment in adapting the economy to climate change is expected to be no less impressive. Developing economies alone will need $100 billion-$180 billion. This means the overall size of capital investment will most likely exceed 0.5 percent of global GDP.

World Bank forecasts suggest that investment in adapting the global economy to climate change may reach $75 billion, while investment in the reduction of greenhouse emissions and other preventive measures may reach $400 billion a year, or 0.30% to 0.32% of global GDP. However, if one considers the fact that all these forecasts operate on median figures only while the actual parameters vary from $30 to $90 billion and from $140 to $675 billion respectively, then some expenditures, like cleaning up from natural disasters, are underestimated. The actual cost of large-scale projects usually exceeds the initial calculations by a factor of at least two; the size of capital investment in the mitigation of climate risks for the world economy will be close to or surpass an average annual 0.5 percent of GDP.

The latter figure is considerably larger than a forecast by Nicholas Stern’s research group, whose 2006 publication on the economic aspects of climate change remains the sole and most authoritative source. The researchers believe that aggregate spending (investment plus capital expenditure) for reducing greenhouse emissions during the period up until 2030 will not exceed 0.10 or 0.11 percent of global GDP – which is not at all small, since it actually translates into hundreds of billions of dollars.

Yet the size of investment as such is not the main problem. Much more important is the ecological imperative; i.e. how much is needed right now and in which particular projects for climate risk management should be invested. Also important is the social and economic efficiency; that is, it is crucial to determine sectors of the economy and fields of activity, production and services that will be the most promising in terms of investment for supporting steady prospective growth rates and economic modernization.

CAUSES OF CLIMATE CHANGE AND THE ECONOMIC POLICIES FOR MITIGATION ITS AFTERMATH

The answers to the questions mentioned above are directly linked to an analysis of the causes of climate change. This analysis underpins, in part, the decisions regarding what economic agents should do and which of them should do it, and also who should pay for the things to be done.

If you recognize the prevalent role of anthropogenic factors in climate change, this means that at the global level developing countries really have plausible arguments to apportion responsibility to industrialized nations for the two hundred years of industrial activity and the ensuing growth of concentrations of greenhouse gases in the atmosphere. But if the concept of natural changes in climate is adopted, the solution to the problem lies in the active involvement of all parties concerned, rather than in the responsibility of a particular group of states.

The premise about historical responsibility needs a reservation. The most recent research into the impact of the types of soil development on climatic change has shown that slash-and-burn practices, which are still widely practiced in developing nations, constitute a sizable – and unacknowledged until very recently – contribution to the growing emissions of greenhouse gases. Thus the role these countries have played in global warming takes on a new dimension, although the politicization of such research is hard to escape, considering the fact that it was done by experts from the U.S. and the EU.

At the state level, recognition of the dominant role of anthropogenic factors among the causes of climate change means that it is crucial to address the problem of the so-called external costs, which implies placing emphasis on investment and technological programs for reducing greenhouse gas emissions. The cost should be established either through market – including exchange markets – trading (in which case companies and industrial enterprises, especially privately owned ones, become the main regulators), or through the introduction of taxes on these emissions, which is the prerogative of the state. It should be noted that state institutions – above all, legislation stipulating the rules of conduct for market players – have a significant role in the case of market estimation of the costs, as well.

The situation differs markedly, however, if we accept the omnipotent role of natural climate change. In this case the main strategy would be to adapt the world’s population and economy to climate change, in which the state would have a priority role. Correspondingly, the responsibilities and financial burdens involved in responsive measures to climate change would differ significantly.

Presumably, the most relevant is the concept of combined anthropogenic/natural causes of the acceleration and intensification of climate change over the past fifty to sixty years. However, this approach raises a new fundamental question, namely, the assessment of the correlation between anthropogenic and natural factors. For investors, most important is the assessment probability degree, which directly correlates with the degree of capital investment risk. An instance of this is found in the IPCC Fourth Assessment Report, released in 2007, which states a very high (more than 90 percent) probability that anthropogenic factors play a “crucial” role (which the document does not specify). If we make a supposition that the probability equals 0.91 and the impact (which is not specified) reaches 55 percent – a figure perfectly matching the postulations made in the report – then the correlation between the anthropogenic and natural factors stands at 50/50.

This assessment makes the risks of such investment really large. What has been said above underlines the complexity of working out an efficient economic strategy with regard to risks from climate change that would envision a system of priorities and multi-stage echeloning when the risks are hedged.

If one puts this hierarchy of priorities into practice, the state should have both the key role in creating incentives for attracting private capital and the role of the major investor. In choosing among investment programs, preference should be given to those which link capital investment to the reduction of climatic risks and economic development per se. No less important is the task of increasing financing and raising the prestige of science, since the progress of the latter helps implement the “precautionary principle” which proceeds from the assumption that even if the impact of anthropogenic factors is very small, it should be reckoned with in decision-making.

Current data does not make it possible to tell if this impact is “the last drop” that will trigger a sharp change in the existing climatic regime, and the ensuing impact on human health and the economy. The precautionary principle is stipulated, for instance, in the UN Framework Convention on Climate Change. The problem is that it raises objections among economic liberalists, including Russian ones. They assert that abiding by this principle may divert investment from the production industries and from making extra profits.

In actual fact, we should talk about multi-functionality or, as economists say, the multiplier effect of investment that should integrate the solution of tasks for Russia’s economic development, the maintenance of growth rates and, most importantly, a marked overhaul of the economy and its modernization on the basis of innovation, with the task of reducing climate risks. The industries and areas of activity where the aforesaid effects can be achieved fairly soon are well known. This is, above all, the energy infrastructure and the related R&D whose multiplier effect (computed on the basis of the U.S. economy, as no data for Russia is available) is almost twice as high as the average for the economy in terms of an increase in jobs and GDP. Also, there is the housing sector and public utilities, the industries and transport where energy saving measures help generate added value and simultaneously cut down greenhouse gas emissions while operating moderate costs or even saving aggregate costs. However, the current situation and the Russian government’s Concept for Long-Term Social and Economic Development (up until 2030) suggest such a correlation policy has not taken root. Vital as the document is, it does not take account of the ongoing global economic crisis, to say nothing of the risks from climate change.

In the meantime, the changing climate is influencing an active formation of two new segments of the global economy. One of them is the “green economy,” which embraces technologies and the manufacture of equipment that help reduce and control emissions, energy/resource savings, monitoring/forecasting of climate changes, adaptation of buildings and facilities to abrupt changes in temperature, humidity and wind, etc. Estimates put the size of the green economy at $2 trillion, or about 3 percent of global GDP, but in reality its contribution is much bigger if one considers that the relevant production facilities are highly extensive in developed countries.

The share of the green economy is expected to grow considerably in the future. This is shown by a new long-term economic strategy released by the EU, “Europe 2020,” which names the sustained development of a “low-carbon,” resource-efficient and competitive economy as one of three priorities. (The two other strategies are “smart growth,” implying an economy based on knowledge and innovation, and “inclusive growth” which suggests ensuring enough jobs and the social and territorial integration of society.)

The other segment is the so-called “carbon market,” or trading in quotas for greenhouse emissions. Its capacity is not large as yet – about $150 to $160 billion, in which the lion’s share belongs to the European Union Emissions Trading Scheme (EU-ETS). However, its growth shows impressive rates – 200 percent from 2005-2009. Two of these years fell during the global financial crisis, when the carbon market was shrinking together with other commodity markets, although at a slower pace. Some forecasts suggest the capacity of the carbon market may reach $1 trillion by 2020.

Russia should embed itself in both new segments and develop its own clean industries, many of which are at the cutting edge of research and technological progress and embody the very innovations that are so badly needed for Russia’s modernization. These opportunities may be lost if an inertia scenario or a similar one is implemented, then the risk will appear of a widening gap in the levels of competitiveness of the Russian economy and the world’s leading countries, including economies in transition.

CLIMATE CHANGE AS A FACTOR OF RISK FOR THE RUSSIAN ECONOMY

As we said earlier, the rate of temperature changes in Russia outstripped almost twofold the rates demonstrated by other countries over the last century. The warming largely affects northern territories that occupy 60 percent of Russia’s total territory. The degradation of permafrost has spread to 4 million square kilometers, causing changes in the properties of the soil, particularly its load-carrying, and in the related infrastructure. Simultaneously, the ice shield is melting in the seas bordering on Russia.

Russia also accounts for the greater part of the so-called “poles of temperature increase,” which reached 5 to 6 degrees Celsius in the aforesaid period. These poles are located in Altai, the Chita and Irkutsk regions, and in the south of Siberia; that is, in areas that are of strategic significance for production and development of natural resources. Cities like Nadym (one of Russia’s gas centers), Surgut (an oil industry center) or Vorkuta (a coal-mining center) have already begun to experience severe problems, which are likely to get worse in the coming decades.

Also evident is the tendency towards a decrease in atmospheric precipitation and the ensuing frequent droughts over an area of about 15 or 16 percent of Russian territory. This concerns the southern part of Western Siberia, the Rostov region, the Stavropol region and Krasnodar Territory – Russia’s major “grain baskets.” The detrimental consequences for agriculture and the risks for food security are all too obvious. The decrease in precipitation results in a growing fire hazard. A rise in air temperature by one degree Celsius increases the number of forest fires and expands their area and period by an average of 12 to 16 percent.

At the same time, the greater part of Russian territory – 80 or so percent – is likely to see a growth in atmospheric precipitation, resulting in more powerful spring floods, inundations and land submerged under water. The Ministry for Emergency Situations /EMERCOM/ says Russia has only two-thirds of the water engineering /hydrotechnical facilities it needs. Of that amount, 70 percent of the facilities are in very bad physical condition. Intensive precipitation leads to water-logging, which in its turn is fraught with outbreaks of epidemics. The rise in temperature levels affects people’s health. About 2,000 people died of heat stroke in Russian cities in the summer of 2003, while in Europe the figure stood at around 50,000. Wind speeds are changing as well, which is accompanied by hurricanes, storms, etc.

The sectors of the economy most sensitive to weather change account for about one-third of GDP. These include agriculture, forestry, water resource systems, transport, tourism, the spa industry and some other areas. Their annually losses from the current trends in climate change in the regions may reach one percent of GDP. The aforementioned Concept for Russia’s Long-Term Social and Economic Development notes the possible emergence of climatic barriers capable of impeding economic growth. Some of these barriers have already appeared.

CLIMATE CHANGE AND NEW ECONOMIC OPPORTUNITIES FOR RUSSIA

The same document points out that climate change opens up windows of opportunity for the Russian economy. Apart from bad impacts, it has some lucrative effects, as well. Above all, this is manifest in a shorter heating season, which is crucial for the energy sector, housing services, public utilities, transport systems, and ordinary consumers. According to a 2009 report by the Federal Service for Hydrometeorology and Environment Monitoring (Rosgidromet) for the Russian government, the heating season is now four to ten days shorter, depending on the territory. This helps save more than 50 million tons of equivalent fuel every season, or 450 billion rubles (in 2009 prices).

In addition, there has been an expansion of arable farmland and the growing season has become longer, which suggests benefits for agriculture and related industries. Also, the melting of the ice cap in the northern territories, mentioned as an unfavorable factor above, expands transportation opportunities. For instance, even a partial freeing of the Northern Sea Route of ice will prolong the shipping season and increase the industry’s potential. The same goes for automobile transport, as a shorter winter yields a reduction of costs incurred in fighting ice on roads. Naturally, these trends have certain probability reservations as nothing can be guaranteed in what concerns climate change.

Not only the lucrative effects of climate change per se but also the tentative effects arising from society’s response to the above-said risks may bring benefits. This is, above all, the willingness to modernize the economy by using new technologies that would alleviate the burden on the environment. Economic modernization programs primarily provide for an increase in the efficiency of the energy sector and energy saving through innovative preventive measures aimed at reducing greenhouse gas emissions. Specifically, the list of critical technologies involved in the modernization program endorsed by Russian President Dmitry Medvedev includes the use of alternative energy sources, transition to new types of transport fuel, etc. Adaptive innovation is the mandatory element of the program; it envisages the use of new materials and new varieties of plants that will help adjust the economy to the new climatic situation. We can and must avoid an additional – and often unnecessary – burden on the environment, given the realization that the variability of nature is not going away.

The economic mechanisms of the Kyoto Protocol (which include joint projects with Western partners and the selling of quotas for greenhouse emissions) may also provide sources for investment. Regrettably, these mechanisms remain untapped. As a result, Russia lost about $2 billion that it could have used for modernizing energy facilities. Russia will still have a chance to attract investment before the Kyoto Protocol expires in 2012 despite the fact that its competitors – mainly China – have seized a sizable share of the market. Let us be clear: contrary to allegations in some of the mass media, the case in hand is not trading in air. The situation offers a tangible opportunity to get direct investment and technologies that will help Russia with the structural overhaul and modernization of its economy. Specifically, they will help get rid of the dominating speculative portfolio investments that have flooded the country in the recent past. It was their flight from Russia that largely contributed to the financial and economic crisis in this country.

Generally, crises have badly impacted the rates of and prospects for economic modernization that are linked to energy savings and energy efficiency, and that are stimulated, in part, by climate change. And yet it often happens that a crisis also provides an impulse towards development, first and foremost, to search for new spheres of investment – the economic niches where capital investment will produce the biggest yield and the biggest multiplicative effect in the short and mid-term. As for the long term, this may help reach the levels of modernization that will ensure steady growth and produce the buds of a new technological system. In this sense, technologies facilitating the solution of problems arising from climate change prove to be the instruments that help attain the greatest multiplicative effect.

It is important to note that the anti-crisis programs of industrialized countries and countries in transition – and Russia is one of them – attach significant importance to the modernization of energy and transport infrastructures, the development of alternative sources of energy and related R&D. Spending on these purposes in national anti-crisis packages has reached 81 percent in South Korea, 38 percent in China, 21 percent in France, and 12 percent in Germany and the U.S. As for Russia, it does not exceed 2 percent.

At the same time, the data in the table below shows that the economies of Russia and other countries have many common opportunities that have not been fully employed so far, especially by Russia.

It is clear that public utilities in Russia and in foreign countries can score results in energy savings and the reduction of greenhouse gas emissions, as they account for almost one-fourth of the total output. This is precisely the segment of the economy where investment has the biggest and the earliest yield. Many researchers underline this link in the resolution of financial and climatic crises. The scope includes authoritative personalities like Nobel Prize winner Joseph Stiglitz and Nicholas Stern, who published an article about this in the highly pragmatic The Financial Times in early March this year.

* * *

Climate change is a new factor in the development of the global and Russian economy. It can have highly diverse aftermaths: it may exert negative impacts and create losses for some groups of the population, industries and regions, while at the same time produce favorable effects from which some economic actors stand to win. According to assessments by U.S. experts, the balance of different climate effects is advantageous for Russia: it is probably the only country that stands to gain an additional 0.6-percent growth in GDP after 2050. Such conclusions look premature. Experience and model calculations show that global climate typically displays unexpected abrupt changes accompanied by substantial damage to people’s health and the economy. The territories that fairly recently would have been considered as beneficiaries of climate change may turn into problem areas. But there are no grounds for excessive alarm either.

In spite of the highly controversial picture of climate change, it is fairly clear that already in the near future all world countries will increasingly employ climate change as a pretext for shackling their counterparties and stimulating their own producers in the competition for a speedy transition to new technological systems in the economy. This will involve, above all, the “Golden Billion” countries and the fastest-growing BRIC economies. It would be highly desirable to see Russia successfully overcome the hydrocarbon barriers erected in its way in the form of draconian fees for its major exports, mainly represented by products received with the help of resource and energy intensive technologies and massive emissions of greenhouse gases.

The risks ands benefits of climate change require a transition to long-term planning, as the climatic factor is long-term by virtue of its nature. In other words, Russia faces a climatic or, in a broader sense, ecological challenge of turning to a genuinely strategic type of planning. This in its turn will entail working out a set of requirements for drafting critical programs for the country’s development and adjusting considerably the state statistics system.

It is also critical to review the attitude towards science, which provides the only efficient instrument for scaling back the uncertainties arising from climate risks and specifying the ways for the economy’s adaptation to climate change. These are sciences studying the Earth, including hydrometeorology disciplines, engineering and technology theories, and economics that should provide accurate accounting and assessment of all aspects of economic development, with regard to climate and other risks.

In foreign policy Russia must definitely use the potential of international cooperation, remembering that if you are not present at the negotiation table you run the risk of finding yourself “on the menu.” We must use the opportunities offered by the hydrocarbon market and take account of its risks. Finally, it would make sense to introduce amendments to the recently adopted National Security Strategy with regard to geopolitical, political and economic factors of global climate change.